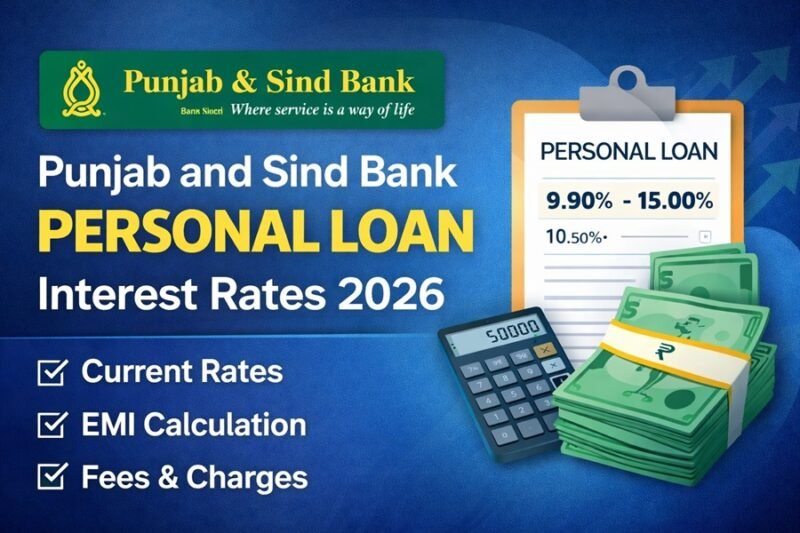

Punjab and Sind Bank personal loan interest rates range between 9.90% and 15.00% per annum depending on loan amount and credit profile. The bank offers loans up to ₹15 lakh for a maximum tenure of 60 months.

Punjab and Sind Bank offers personal loans at interest rates starting from 9.90% per annum, with loan amounts up to ₹15 lakh and repayment tenures extending to 60 months. The bank provides competitive rates for both salaried employees and self-employed professionals, with processing fees of 1% of the sanctioned amount.

Punjab and Sind Bank Personal Loan Interest Rates and Charges

| Loan Amount | Interest Rate (p.a.) | Tenure | Processing Fee |

| Up to ₹3 lakh | 9.90% – 14.50% | 12-60 months | 1% of loan amount |

| ₹3 lakh – ₹7 lakh | 10.25% – 14.75% | 12-60 months | 1% of loan amount |

| ₹7 lakh – ₹15 lakh | 10.50% – 15.00% | 12-60 months | 1% of loan amount |

Additional Charges:

- Prepayment charges: 2% on outstanding principal

- Late payment penalty: ₹500 per instance

- Cheque bounce charges: ₹350 per cheque

- CIBIL report charges: ₹100 (one-time)

Note: Rates are subject to change based on RBI guidelines and applicant’s credit profile. Last updated: April 2024.

Eligibility Criteria

For Salaried Employees

- Age: 21 to 60 years

- Minimum monthly income: ₹15,000

- Work experience: At least 2 years, with 1 year in current organization

- Employment type: Permanent employee in a government body, PSU, MNC, or reputed private company

For Self-Employed Professionals

- Age: 25 to 65 years

- Business vintage: Minimum 3 years

- Annual income: At least ₹3 lakh

- ITR filing: Last 2 years mandatory

Credit Score Requirements

Punjab and Sind Bank prefers applicants with a CIBIL score of 700 or above. Applicants with scores between 650-699 may receive approval at higher interest rates. Those below 650 typically face rejection.

Documents Required

Salaried Applicants

- Identity proof: Aadhaar card, PAN card, passport, or voter ID

- Address proof: Utility bills, rental agreement, or passport

- Income proof: Last 3 months’ salary slips and 6 months’ bank statements

- Employment proof: Appointment letter and employee ID card

- Passport-size photographs

Self-Employed Applicants

- Identity and address proof (same as above)

- Business proof: Registration certificate, GST registration, or shop establishment license

- Income proof: ITR for last 2 years with computation of income

- Bank statements: Last 6 months of business account

- Business address proof: Electricity bill or property tax receipt

EMI Calculation Example

Let’s calculate the EMI for different loan scenarios:

Scenario 1: Mid-range loan

- Loan amount: ₹5 lakh

- Interest rate: 10.50% p.a.

- Tenure: 36 months

- Monthly EMI: ₹16,179

- Total interest paid: ₹82,444

- Total amount payable: ₹5,82,444

Scenario 2: Higher loan amount

- Loan amount: ₹10 lakh

- Interest rate: 11.00% p.a.

- Tenure: 60 months

- Monthly EMI: ₹21,742

- Total interest paid: ₹3,04,520

- Total amount payable: ₹13,04,520

These calculations help you understand the actual cost of borrowing. A longer tenure reduces your EMI but increases total interest paid.

Processing Fees and Hidden Charges

Punjab and Sind Bank charges 1% of the sanctioned loan amount as processing fee, which is lower than many private banks. However, watch out for these additional costs:

Upfront Costs

- Processing fee: 1% (non-refundable)

- CIBIL report charges: ₹100

- Stamp duty and documentation: Varies by state (₹500-₹2,000)

Ongoing Charges

- Late payment penalty kicks in after 3 days of due date

- Part-prepayment allowed after 12 EMI payments

- Full foreclosure permitted anytime with 2% charge on outstanding principal

Hidden Costs to Watch

Some branches may suggest loan insurance, which is optional. This can add 0.5-1% to your annual cost. Evaluate whether you need this coverage before agreeing.

Special Benefits and Features

PSB Samridhi Personal Loan

Punjab and Sind Bank offers a special scheme for pensioners with reduced rates starting at 9.70% p.a. This product targets retired central and state government employees.

Quick Disbursal

Pre-approved customers receive funds within 48 hours of document submission. New customers can expect disbursal within 7-10 working days.

Flexible Repayment

The bank allows you to increase EMI amount during the tenure, helping you close the loan faster without prepayment charges on the increased portion.

Balance Transfer Option

Existing personal loan borrowers from other banks can transfer their loans to Punjab and Sind Bank at competitive rates, subject to eligibility.

Comparison with Similar Government Banks

| Feature | Punjab and Sind Bank | Bank of Baroda | Union Bank of India |

| Interest Rate | 9.90% – 15.00% | 10.25% – 15.35% | 10.30% – 15.05% |

| Maximum Amount | ₹15 lakh | ₹20 lakh | ₹15 lakh |

| Processing Fee | 1% | 0.50% – 2% | Up to 1% |

| Tenure | Up to 60 months | Up to 60 months | Up to 60 months |

| Prepayment Charges | 2% | 2% – 4% | 2% |

Key Differentiators

Punjab and Sind Bank offers mid-range rates among government banks. Their approval process takes slightly longer than private lenders but remains faster than most PSU banks.

Bank of Baroda provides higher loan amounts and occasionally runs promotional campaigns with reduced processing fees. Their interest rates start marginally higher but may be negotiable for high-value customers.

Union Bank of India maintains rates similar to Punjab and Sind Bank but has stricter eligibility norms for self-employed applicants.

Who Should Apply

Ideal Candidates

- Government employees seeking lower rates

- Salaried professionals with stable income and good credit scores

- Borrowers looking for transparent fee structures

- Those who prefer government bank security over private bank speed

- Pensioners eligible for special schemes

Strong Application Profile

Your application stands stronger if you:

- Maintain a CIBIL score above 750

- Have existing relationship with Punjab and Sind Bank

- Show regular savings pattern in bank statements

- Work in PSU, government department, or reputed MNC

- Apply for loan amount within 3x your monthly income

Who Should Avoid

Consider Alternatives If You

- Need instant approval and same-day disbursal (private banks are faster)

- Have CIBIL score below 650 (approval chances are slim)

- Are self-employed with irregular income documentation

- Require loan amount above ₹15 lakh

- Prefer completely online application process

Better Options Exist For

- Startup founders: NBFCs offer more flexible criteria

- Young professionals: Fintech lenders provide app-based convenience

- High-income earners: Private banks negotiate better rates for premium customers

- Irregular income: P2P lending platforms assess beyond traditional parameters

Frequently Asked Questions

Can I apply for Punjab and Sind Bank personal loan online?

Punjab and Sind Bank requires you to visit a branch for personal loan applications. While you can check eligibility online, document submission and verification happen in person. The bank has not yet introduced a fully digital application process.

What is the minimum salary required for a personal loan?

Salaried employees need a minimum monthly income of ₹15,000 to qualify. This requirement applies to gross salary before deductions. Self-employed professionals must show annual income of at least ₹3 lakh through ITR.

How long does loan approval take?

Pre-approved customers receive approval within 2-3 working days. New applicants should expect 7-10 working days for complete processing, including document verification and credit assessment. Disbursal happens within 48 hours of final approval.

Are there any special rates for existing customers?

Yes. Customers maintaining salary accounts or holding deposits with Punjab and Sind Bank may receive a rate reduction of 0.25% to 0.50%. The exact discount depends on your relationship value and negotiation with the branch manager.

Can I prepay my personal loan without penalty?

Part-prepayment is allowed after completing 12 EMI payments, with a 2% charge on the prepaid amount. Full foreclosure is permitted anytime but attracts 2% charge on the outstanding principal. The increased EMI facility allows faster repayment without these charges.

Content Navigation Suggestions

Related topics you might find useful:

- “How to improve CIBIL score for personal loan approval”

- “Personal loan vs credit card: which is cheaper for emergency expenses”

- “Government bank vs private bank personal loans: detailed comparison”

- “Step-by-step guide to calculate personal loan EMI manually”

- “Top 5 reasons for personal loan rejection and how to avoid them”

Making Your Decision

Punjab and Sind Bank personal loan interest rates remain competitive within the government banking sector. The bank suits borrowers who prioritize transparent pricing and regulatory safety over processing speed.

Check your credit score before applying. Compare final costs including all fees, not just advertised interest rates. Calculate your EMI against monthly income—keep it below 40% of take-home salary for comfortable repayment.

Visit your nearest Punjab and Sind Bank branch with complete documentation. Ask about any ongoing promotional offers. Negotiate rates if you maintain substantial deposits or have an existing relationship with the bank.

Financial Disclaimer: Interest rates, fees, and loan terms mentioned are indicative and subject to change based on RBI guidelines and individual credit profiles. Verify current rates with Punjab and Sind Bank directly before making borrowing decisions. This content is for informational purposes and does not constitute financial advice.